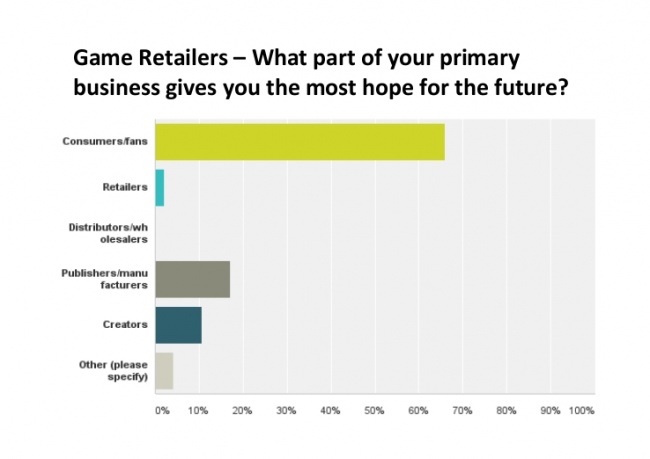

This is a much stronger positive sentiment than is held by comic retailers, for which we reported survey results yesterday (see "Comic Retailers Confident about Customers, Concerned about Publishers").

The next highest number of choices when to parts of the business that make the products retailers sell. Over 15% of game retailers chose "publishers/manufacturers," and around 10% chose "creators" when asked what part of their primary business gives them the most hope for the future.

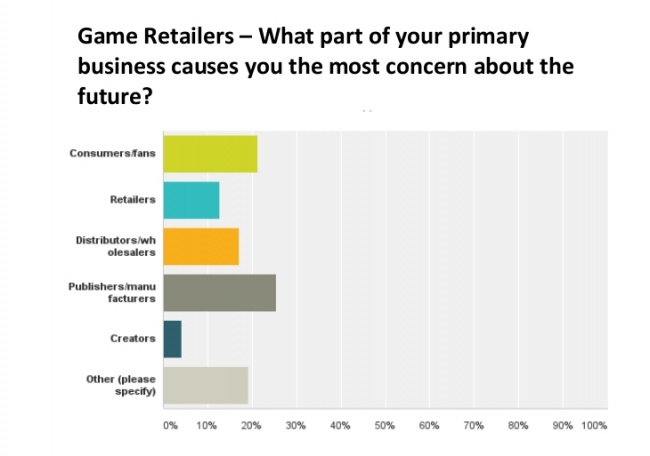

Consumers/fans, "other," and distributors/wholesalers were each chosen by around 20% of game retailers as the part of the business that caused them the most concern, with almost all of the "other" respondents describing some form of online competition, also a source of concern for a significant percentage of comic retailers.

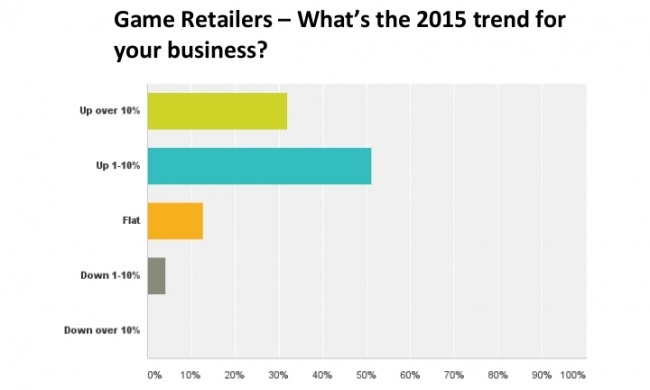

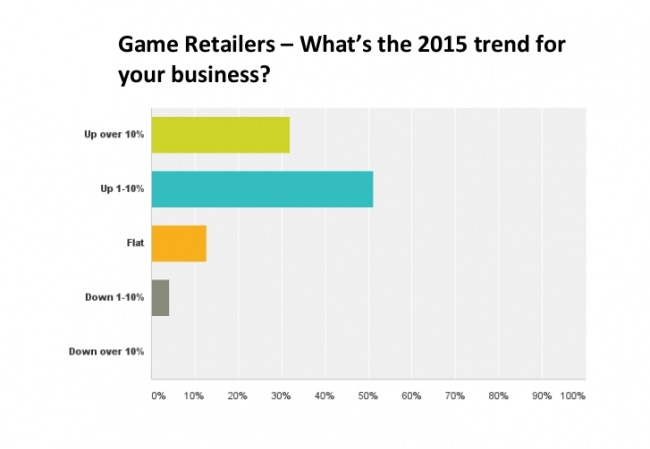

Survey respondents were recruited via multiple channels (ICv2 email, editorial, and advertising) during November 2016. To qualify for this sub-group, respondents had to self-identify as retailers and describe games as their primary business (biggest category in dollars). Given that the sample is self-selected and relatively small relative to the size of the population, it may differ significantly from the actual situation for game retailers as a whole.

Click any image for larger view or see the graphs in the gallery below.

View Gallery: 3 Images

View Gallery: 3 Images