We define "hobby games" as those games produced for a "gamer" market, generally (although not always) sold primarily in the hobby channel of game and card specialty stores. We define the "hobby games market" as the market for those games regardless of whether they’re sold in the hobby channel or other channels. Our estimates include sales in the U.S. and Canada.

The total hobby games market estimate is derived from estimates for five individual categories: collectible games (which include Trading/Collectible Card Games, Collectible Miniatures, and other collectible formats), miniatures (non-collectible), board games, card and dice games, and roleplaying games.

Our primary means of collecting data about hobby games sales is interviews with key industry figures with good visibility to sales in various subcategories and channels. We also review data released by publicly traded companies, publicly available Circana data, and crowdfunding data and analysis.

These estimates should be regarded as preliminary. For the full ICv2 White Paper presentation that first presented these trends, see "ICv2 Hobby Games White Paper 2025." For last year's presentation, see "Hobby Games White Paper 2024").

2024 Trends

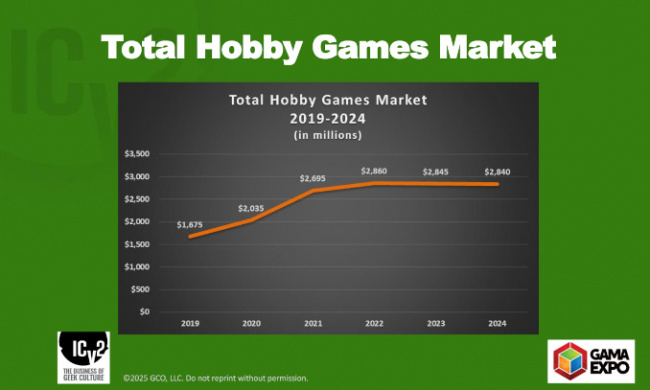

We estimate hobby game sales in the U.S. and Canada at around $2.84 billion for 2024, nearly identical to the $2.845 billion in sales we estimated for 2023, with some minor rotation between categories. One overall trend was the lack of big new hits in the year, which was the case across categories. There were definitely solid product introductions in 2024, but no blow-out hits that changed the business.

Consumers

Consumers were still buying in 2024, despite growing challenges. The biggest challenge was to disposable income, particularly from inflation, which meant that necessities, particularly housing and food, were taking bigger shares of consumer budgets. The demand for community remains a key driver of consumer behavior, a holdover from Covid lockdowns and the rewarding return to in-person shopping and gaming that followed.

Publishers

Publishers struggled to get noticed in 2024, with growth in the number of TCGs, a continuation of large numbers of board game releases, and a ton of small box games all competing for attention from retailers and consumers.

Retailers

Hobby game stores came out of 2024 generally healthy in a manageable environment, with store counts flat to up in the year. While there were definitely challenges due to changing tastes, retailers have generally adapted well to the post-Covid market conditions.

As a result, we estimate that 2024 was the 16th consecutive year of hobby channel growth, at around a 2% rate. The hobby channel increase was driven by minis and RPGs.

Crowdfunding

Crowdfunding appeared relatively flat in 2024. Kickstarter reported worldwide pledges to successful projects at $220 million in 2024, down marginally from the $226 million estimated by third parties for 2023. Meanwhile, Gamefound is growing in importance. As of early 2022 when Ravensburger invested in the platform, only $22 million had been raised to date (see "Ravensburger Invests"); in 2024, Gamefound reported over $85 million in tabletop games pledges.

By Category

While sales of collectible games, the largest hobby games category, declined in 2024, and sales of RPGs grew, the relative shares of the different hobby games categories were relatively stable, with TCGs still making up over half of hobby games dollars.

For the In-depth version of this article, see "In Depth – 2024 Was a Year of Stabilization."

Click Gallery below for full-size charts and graphs!

View Gallery: 2 Images

View Gallery: 2 Images